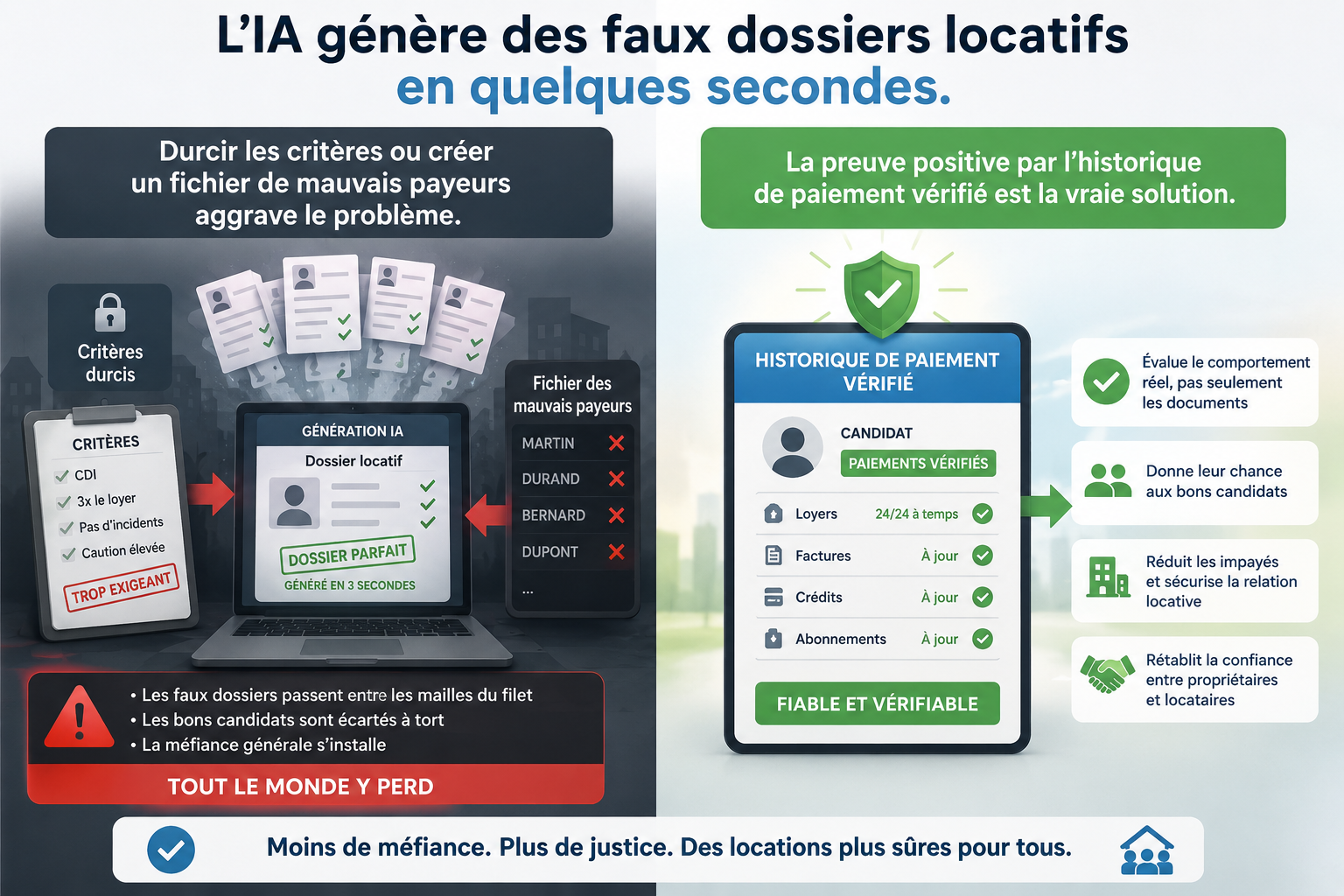

The right response to AI-generated document fraud is not to make selection criteria more stringent, nor to create a blacklist of bad tenants. It's to change the logic: shift from the presumption of reliability based on falsifiable documents to proof of actual payment behaviour, observed over time.

Why Are Fake Rental Applications Exploding in France?

The French rental market is under extreme pressure. In the most competitive areas, demand far exceeds available supply, and the pressure on prospective tenants has become so intense that some cross the line. According to a study conducted by FLASHS for Zelok in June 2025 among 2,000 French people, 26% of tenants admit to having provided inaccurate information in their application. Among 18-24-year-olds, 21% admit to having submitted an inflated payslip and 19% a falsified employment contract.

This practice is not the result of widespread criminal intent. It's a response to a selection system that has become so demanding that it mechanically excludes a large proportion of otherwise reliable candidates. Payslips are the most frequently falsified documents, followed by employment contracts and tax notices. And today, generative AI has changed the scale of the problem: a visually flawless document can be created in seconds, without any special technical skills.

The consequence is direct for landlords and agencies: a visually "clean" document is no longer a guarantee of authenticity. Manual verification, however rigorous, reaches its limits when faced with increasingly sophisticated falsifications.

Prove your rental reliability, or verify a candidate's

Tightening Selection Criteria: A False Good Idea

Faced with this reality, the market's instinctive reaction is to raise the barriers: require a permanent employment contract (CDI), a guarantor, income representing three or four times the rent amount, or both simultaneously. This logic is understandable, but it produces two well-documented perverse effects.

First effect: it excludes reliable tenants with atypical profiles. A self-employed person with ten years of stable activity, a performing arts professional who has paid rent without fail for years, a pensioner with modest but regular income, or a candidate returning from abroad without a French tax notice, all find themselves excluded not because they are bad payers, but because their documents don't match the expected model. A user's comment on a rental manager forum sums up the situation well: "NO ONE will rent to me, not even mouldy dumps, despite €4,000 in monthly income", for lack of standard payslips.

Second effect: it fuels the fraud it claims to combat. The higher and more rigid the criteria, the more the candidate who doesn't naturally meet them is incentivized to circumvent them. By systematically requiring a CDI with several times the rent, the market itself creates demand for fake documents. Falsification becomes a rational response to requirements perceived as arbitrary.

The Bad Tenant Blacklist: A Double-Edged Negative Logic

The other response proposed by some industry players is the creation of a file listing tenants with rent arrears, accessible to real estate professionals. In France, the so-called "Arthel list" project, supported at one point by the FNAIM, crystallized this debate. It was ultimately abandoned in the face of widespread opposition.

The National Housing Confederation (CNL) denounced this file as "an invasion of privacy and an additional barrier to housing access". The CNIL (French data protection authority) recalled the importance of GDPR compliance and expressed reservations about the risks of discrimination and stigmatization. The CLCV consumer protection association judged such a file "a source of discrimination and stigmatization".

Beyond the controversy, the logic of this type of tool presents a structural weakness: it identifies after the fact past defaulting behaviour, without allowing positive recognition of past reliable behaviour. A tenant absent from the file is not proven reliable, they are simply not flagged. This is not the same thing.

Moreover, this type of file mechanically creates market segmentation: on one side the so-called "premium" profiles that agencies compete for, on the other the uncovered or flagged profiles who find themselves pushed towards the least regulated segments of the rental market, precisely where fake applications proliferate most easily.

Open Banking: The Data That Cannot Be Falsified

There is another way. It rests on a simple observation: if declarative documents are falsifiable, transactional banking data comes directly from the bank. It doesn't pass through an editable PDF. It doesn't depend on the good will of a fictitious employer. It reflects what actually happened, month after month.

This is precisely what the European PSD2 directive, which came into force in France in 2019, enables. This regulation governs Open Banking: with the explicit and revocable consent of the account holder, a licensed provider can access payment banking data in read-only mode via a secure API. No writing, no fund movements, no visibility on savings or expenses other than those explicitly shared.

Applied to rental, this channel allows answering the only question that really matters to a landlord: has this candidate paid their rent, on the scheduled date, over a given period? No presumption, no extrapolation from an employment contract: a direct observation of actual payment behaviour.

For KYC and income verification, Open Banking has indeed become, according to industry specialists, "the most reliable route" precisely because the data is "received directly from the bank, without risk of PDF document fraud".

The Tecto Score: Positive Proof, Not Presumption

It is on this logic that ImmoTecto has built the Tecto Score. This is not about assessing what a tenant is supposed to be able to pay based on declarative documents. It's about certifying what they have actually paid, in fact, over an observed period of up to five years.

The Tecto Score analyzes only rent payment behaviour: the actual payment date compared to the contractual due date. Nothing else. Not income, not expenses, not savings, not account balance, not type of employment contract, not nationality, not age. The score ranges from 0 to 100, with up to 10 bonus points: +3 for detecting a standing order for rent payment, +7 for banking loyalty of more than 12 months. It is presented in readable labels: Excellent, Very Good, Good, Average, Needs Improvement.

Three collection channels are cumulative, at the tenant's choice:

- Open Banking connection (PSD2, read-only, initiated and revocable by the tenant), which gives the Verified level.

- Import of account statement in PDF or CSV format, analyzed by our AI for concordance check, which gives the Basic level.

- Screenshots from the banking app, also subject to our AI's concordance check, Basic level.

The combination of all three channels reaches the Certified level, the highest. Seniority stars indicate the depth of history: one star for 1 to 12 months, two stars for 13 to 18 months, three stars for 24 months and beyond. Recent payments are weighted more heavily in the calculation.

For candidates without rental history, a first-time tenant variant is available.

What the Tecto Score is not: it does not constitute a guarantee of future payment, nor rent guarantee insurance. It certifies payment behaviour observed over a given period, based on data verifiable in real time by ImmoTecto servers. It's proof, not a promise.

In accordance with anti-discrimination regulations applicable in France, the Tecto Score can never be the sole criterion for selecting a tenant. The tenant has a right of explanation, contestation and human review, as provided by Article 22 of GDPR. The professional only sees what the tenant has explicitly chosen to share, section by section.

How Does the TectoPass Work in Practice for Agencies and Landlords?

The score is integrated into the TectoPass, a certified and portable PDF passport that the tenant generates at €0. This document is instantly viewable by QR code or digital code, without requiring an ImmoTecto account for the professional viewing it. It contains the Tecto Score, validated documents, guarantors and punctuality history.

The TectoPass is valid for 40 days and regenerable for 3 months. The tenant chooses precisely what they share, section by section, and sees who has viewed their pass. The process is entirely initiated by the tenant: they are the one who builds their file and chooses to prove their reliability, which constitutes the legal basis of the model.

For agencies, the Access plan (from €99 excl. VAT/month) allows TectoPass verification by QR code or code. The Starter and Premium plans provide access to listing publication and, for the Premium plan, to the tenant directory allowing direct search and contact with already-verified tenants. For landlords, an Essential offer at €59.99 incl. VAT in single payment allows publishing one listing and accessing three TectoPass consultations. Full details are available on our pricing page.

Positive Proof Logic vs. Negative File Logic

The distinction is fundamental. A bad tenant file starts from a positive presumption: everyone is reliable until proven otherwise. Proof to the contrary always comes too late, after a rent arrear, after legal proceedings, after damage has been done.

The Tecto Score reverses this logic. It asks the prospective tenant to positively prove their reliability from observable data, even before the lease is signed. No presumption, no stigmatization, no default exclusion of atypical profiles. A self-employed person who has paid rent for three years on a fixed date obtains a high Tecto Score, regardless of their payslips. It's the reality of their behaviour that speaks, not the form of their employment contract.

This is precisely the paradigm shift that ImmoTecto advocates: fewer documents that can be falsified, more data that can be verified.

Are you a landlord, property manager or tenant? Discover how to build or view a certified file via the TectoPass or learn more about how it works. For agencies, consult our dedicated offers.

FAQ

Does the Tecto Score guarantee that a tenant will pay their rent?

No. The Tecto Score certifies payment behaviour observed over a given period, up to five years of history. It proves past reliability from data verifiable in real time, but does not constitute a guarantee of future payment nor rent guarantee insurance. It's proof, not a promise.

Does the Open Banking connection give access to all the tenant's banking data?

No. The Open Banking connection is initiated by the tenant, in read-only mode, and governed by the PSD2 directive. ImmoTecto only analyzes rent payments: not income, not expenses, not savings, not balance. The tenant can revoke access at any time.

Can a tenant without a permanent contract obtain a good Tecto Score?

Yes. The Tecto Score takes into account neither the type of employment contract, nor income, nor any socio-demographic criteria. Only rent payment behaviour is analyzed. A self-employed person, a performing arts professional or a pensioner who pays their rent on a fixed date can obtain an Excellent score.

Does the Tecto Score replace other tenant selection criteria?

No, and this is a non-negotiable legal point. In accordance with anti-discrimination regulations applicable in France, the Tecto Score can never be the sole selection criterion. It complements the tenant file, not replace it. The tenant has a right of explanation and contestation (Art. 22 GDPR).

How much does the Tecto Score cost for a tenant?

Platform access, file building, Tecto Score calculation and TectoPass generation are at €0 for the tenant, with no subscription. ImmoTecto's monetization is exclusively B2B, from agencies and landlords.

Sources

- FLASHS study for Zelok: 26% of tenants admit to having provided inaccurate information in their application, Foncia / Zelok / FLASHS, 2025, study

- Fake tenant file 2026: detect and verify, Foncia, 2026, press

- 2025-2026 trend: fake documents are increasingly professional thanks to generative AI, Docapass, 2025, report

- Forgery and use of forgery: article 441-1 of the Criminal Code, 3 years imprisonment and €45,000 fine, Proplio / French Criminal Code, 2025, official

- Bad tenant payers: soon to be listed? Arthel list and reactions (CNL, CLCV, CNIL), Kaliz, 2022, press

- The creation of a national file of bad tenant payers divides, La-loi-pinel.com, 2023, press

- Is There a Blacklist of Bad Tenant Payers?, BailFacile, 2025, report

- Open Banking & KYC: what PSD2 changes for your journeys in 2026, Datakeen, 2026, report

- Open banking in France, ACPR Survey 2024, ACPR / Banque de France, 2025, official

- Open Finance in the service of Credit Scoring, Centre des Professions Financières, 2024, study

- Housing crisis in Île-de-France: fake applications explode, MySweetimmo, 2026, press

- Housing: the hunt for fake rental applications, France Info / France 2, 2025, press

Ready to rent with confidence? Get your Tecto Score or verify a candidate

Available in other languages

Related articles

Lease Registration in Belgium: Complete Guide 2026

Who must register the lease in Belgium, within what timeframe, with which service and what penalties does the landlord face? Overview by region and practical advice for tenants and landlords.

RéglementationRental Deposit in Belgium: Complete Regional Comparison 2026

Amounts, forms, deadlines and recourse: everything tenants and landlords need to know about rental deposits in Wallonia, Brussels and Flanders in 2026.

RéglementationMain Residence Lease in Brussels: The Complete 2026 Guide

Lease terms, rental deposit capped at 2 months, notice periods, habitability standards, mandatory registration: everything tenants and landlords need to know about Brussels leases in 2026.